According to our research, Kiwi sole traders spend an average of 6 hours a week and up to $246 a month managing their tax and financial admin.

That’s 312 hours and $3,000 a year that could have been better spent elsewhere!

To help you avoid losing so much time and money on admin in FY 2025/26, we’ve put together this guide on good practices that’ll take some of the stress out of sorting your taxes.

Whether you’re a tax veteran or just starting your self-employed journey, here are a few things you can do to save time and money each week, and make filing taxes as painless as possible. Here we go!

Know what you owe

As a sole trader, there’s a lot to think about when it comes to sorting your taxes.

Not only do you have to calculate and pay your own income tax, you also have to sort GST (if registered), ACC levies, and KiwiSaver contributions (optional) – and ideally save enough for a rainy day. Phew!

Taking the time now to plan it all out could save you a huge headache down the line. Not to mention avoiding interests and fines if you’re late paying the taxes and levies you owe. Yikes!

To help you get started, we’ve put together a handy list of all the bits and bobs you’ll need to be across:

Income tax

Your income tax is calculated by adding up all your sources of income (including salary and wages, self-employed income, investment income etc), and applying your effective tax rate – that is to say, the actual percentage of income tax you owe.

(If you’re lost already, don’t panic – we explain how to calculate your effective tax rate in detail in our guide to tax rates and thresholds.)

At the end of the financial year, you’ll need to report all sources of income, as well as any business expenses you’re claiming in your tax return. From there, the IRD will let you know how much income tax you owe. Pretty straightforward!

But, if you haven’t set aside enough funds to pay your income tax bill, it can get downright gnarly. That’s why it’s useful to calculate what you might owe from the get go, so you can save throughout the year instead of being hit all at once.

💡 You can get a rough estimate of your income tax bill using our sole trader tax calculator.

🙋♀️ … or you can use Hnry, and we sort it all for you. Learn more.

GST

If you earn over $60,000 from your self-employed income in any given 12-month period, then you are required to register for and charge GST.

GST is a tax you collect on behalf of the IRD – it’s not something you pay out of pocket. As soon as you’re registered, you’ll need to add an additional 15% on top of your prices, which you then forward on to the IRD at the end of every GST period.

💡 For more information on your potential GST obligations, check out our monster guide to GST.

Student loan

If you have an outstanding student loan, and you earn over the annual threshold of $24,128, then you’re required to make repayments on that student loan.

Your student loan repayment will be 12% of every dollar you earn above the repayment threshold.

💡 We break it all down in more detail in our guide to student loan repayments.

ACC levies

Alongside your other tax obligations, you’re responsible for calculating and paying the ACC’s three levies:

- the Earner’s levy is charged at a flat rate of $1.67 per $100 of your liable income

- the Working Safer levy is charged at a flat rate of $0.08 per $100 of your liable income

- the Work levy is based on the industry you operate in. The riskier your line of work, the higher this levy will be

💡 Need more information? We have a guide to ACC levies.

KiwiSaver contributions

Okay, it’s really not a tax, and it’s definitely not required – but while we’re talking about things you need to set money aside for, you may want to consider contributing to your KiwiSaver fund.

One huge benefit of putting money towards your KiwiSaver is the government co-contribution – for every $1 you contribute, the government will top up your fund by $0.25, up to a maximum of $260.72 each year.

Another real benefit is the magic of compounding returns. Basically, when you invest in a KiwiSaver fund, you’ll ideally earn returns on the money you invest (there are no guarantees!). The returns are then added to the capital to be reinvested, allowing both to generate further returns.

💡 Check out our full guide to KiwiSaver contributions for more!

How to plan ahead

Now you’re across what you need to set aside, here’s how to go about it.

Step One: Calculate your taxes

Use our income tax calculator to calculate your tax rate, (approximate) ACC levies, and student loan repayments.

If you know exactly how much you’ll make this year, our income tax calculator is a simple and accurate way to calculate the amount of money you’ll need to set aside.

If you don’t know how much you’ll earn, our calculator is a good starting point. Plug in your previous year’s income, and go from there. As your projections for the year change, keep revisiting the calculator to make sure you’re still on track to meet your obligations.

Step Two: Get to grips with GST

Like we said earlier, if you expect to earn $60k in self-employed income in any given 12-month period, you’re required to register for and charge GST. If you’re registered for GST, and you fail to collect it on the IRD’s behalf, you are still be required to pay GST owed – only it’ll be out of your own pocket (oof).

That’s why it’s so important to be across your obligations, to avoid any expensive mistakes. Remember, GST for your services is a tax paid by your customers, not by you!

💡 You can reduce your GST bill by claiming back the GST your business has paid when purchasing goods and services. For more information, check out our guide to GST.

Step Three: Make the most of KiwiSaver

Contributing to your KiwiSaver could help set you up for future financial success. If you can, regular contributions can make all the difference!

If you make personal contributions to your KiwiSaver fund, you may be eligible for a government contribution of up to $260.72 annually. All you have to do is contribute $1042.86 between the 1st of July and 30th of June each year

That’s easy money being left on the table if you’re not taking advantage of it!

🙋♀️ Looking for a way to automate all of the above? Hnry calculates and pays your tax, GST, and ACC levies every time you get paid.

While that’s a heck of a lot to be thinking about, our budgeting journey doesn’t stop there. Let’s look at what else you should be setting aside funds for: planned and unplanned time off work.

Step four: Factor in time spent not earning

The best-laid plans of mice and men, right? Despite our best efforts to reach our business goals, life will sometimes get in the way. We need to make sure we have a rainy day fund to cover both the expected and the unexpected.

Get the ball rolling on this fund by calculating the total number of days a year you might not be able to work. For example:

- Public Holidays: Aotearoa celebrates 11 national public holidays, and one regional public holiday, for a total of 12 days off

- Personal Holidays: Are you taking a vacation this year (you absolutely should)? Do you need some time off to refresh and recharge? Give yourself some ‘annual leave’ and factor ‘paid’ time off into your budget!

- Sick Leave: PAYE employees get 10 sick days a year. Even if you don’t need it, knowing you have 10 days worth of income stashed away can make falling ill less stressful.

- Slow Periods: Many industries have slumps in activity at certain points in the year. If you know when yours are, you can compensate by putting more aside during busy periods.

If possible, it’s always best to err on the side of caution and factor in one or two days extra, just in case of emergencies.

The next step is to estimate how much money you need to set aside in order to cover these potential days off. This amount may vary by type of ‘leave’ – you might want to save more to spend for a vacation than during a sick day, for example – but at the very least, the amount you set aside should cover all your expenses for the time you take off.

📖 For more tips on planning leave, check out our guide to taking time off.

Step five: Regularly set money aside

If you’ve calculated all of the above, and it turns out you have enough savings to cover your taxes and time-off, sweet! Our work here is done, and you can reward yourself with a nice hot/cool drink, depending on the weather.

But if you don’t yet have a fund in place, don’t worry. We can create one. All you need to do is set yourself a savings target based on how much you need, decide on a savings timeframe, and then put money aside each paycheck until you’ve reached your goal. How little or how much you put aside is entirely up to you.

Hnry makes this easy for sole traders by automatically assigning a percentage of their income to a savings account (or wherever they’d like to send it - investments, charities, friends and family, you name it). You can find out more about our automatic allocation feature here.

Get savvy with expenses

Now we get to the fun stuff!

When you claim business expenses, you reduce your taxable income and thus your overall tax bill. But you have to be careful to only claim what you’re allowed to claim - otherwise, you risk playing the IRD lottery.

Find out what you can claim

As a general rule, you can claim a tax deduction for a business expense as long as:

- the expense relates directly to earning income,

- or running your business.

Taking the time now to discover what you can claim as a business expense will set you up for the year ahead. As always, if you’re unsure about what you can claim as a business expense, you’re better off checking with a tax specialist (or if you’re a Hnry customer, the friendly Hnry team!).

📖 For more information, check out our monster guide to business expenses for Kiwi sole traders!

Save your receipts

There’s nothing worse than putting hours of blood, sweat, and tears into your financial admin, only to realise at the end of the financial year that you lost the receipts!

Keeping clear, organised records of purchases and goods/products sold will help make tax time as stress-free as possible. It’s also good practice; the IRD requires you to save a record of your expenses (receipts) for seven years after purchase, either physically or digitally.

Imagine seven years of receipts strewn across your office floor, and you can see why a good filing system is super important!

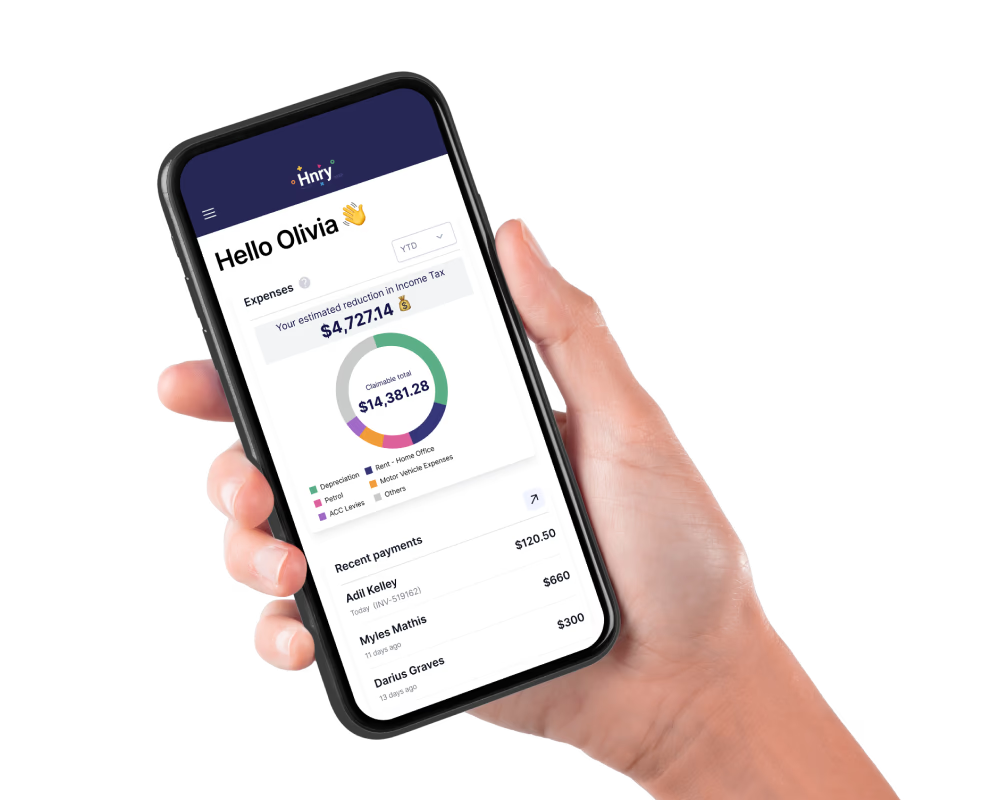

That’s where Hnry comes in. You can raise expenses in our app, and we’ll manage them for you. We calculate your tax savings from expenses as you go, giving you immediate tax relief. Plus, we store your receipt photos for you for the required seven years – no shoebox required, ever again!

For bonus points, you could also use the Hnry Debit Card. Every time you use it to make a purchase, it automatically raises an expense in the Hnry app, so nothing slips through the cracks. From there, all you need to do is upload a pic of your receipt, confirm a few details, and you’re done. Expenses sorted!

Save time, money, and energy with Hnry

We may be biased, but we believe that the best way for sole traders to maximise their tax deductions (legally) is to use Hnry.

Hnry is an award-winning tax app and service that’s helping sole traders spend less time on financial admin, and more time doing what they love (unless what they love is financial admin).

Once you’re up and running with Hnry, we’ll automatically calculate and deduct your:

… every time you’re paid, so you won’t accidentally end up with a massive tax bill at the end of the financial year. We’ll even file your annual tax return for you, at no additional cost.

Raising expenses through our app is as simple as taking a photo of your receipt and inputting a few extra details. From there, our accountants will manage and claim your expenses, so you get the tax relief back in your pocket in real time (rather than having to wait until the end of the financial year). Easy as!

Get your tax ducks (and deductions) in a row by joining Hnry today!