Whether you work for an employer, or own your own business, taxes are unfortunately a fact of life.

As much as it would be nice to keep more of our hard-earned cash, if you’re earning an income, you’re required to pay income tax. Ouch.

To make matters more complicated, figuring out how much you owe Inland Revenue can involve a fair bit of maths. That’s because Aotearoa operates using a progressive tax system with several tax brackets split by income level, rather than a single flat tax rate.

So what does this mean, exactly? Better yet, how can you make the most of this system to (legally) pay less in taxes? Don’t worry, we’ve got you covered. Let’s get stuck in!

What’s a tax rate?

We’re so glad you asked! A tax rate is defined as the ratio between a sum of money and the tax owed on that money, calculated as a percentage. Don’t worry; it’s not as confusing as it sounds.

For example, if you had $100 of taxable income, and paid $10 of that in tax, the ratio between income and tax would be 10:100, simplified to 1:10. This ratio in percentage form is 10% - the tax rate.

If you wanted to simplify that even further, you could take the maths out of it and think of it like this: A tax rate is the percentage at which a person or business is taxed.

Some taxes are easy to calculate – for example, GST (Goods and Services Tax). It’s levied at a flat rate of 15% on top of the cost of most goods and services. Fairly straightforward.

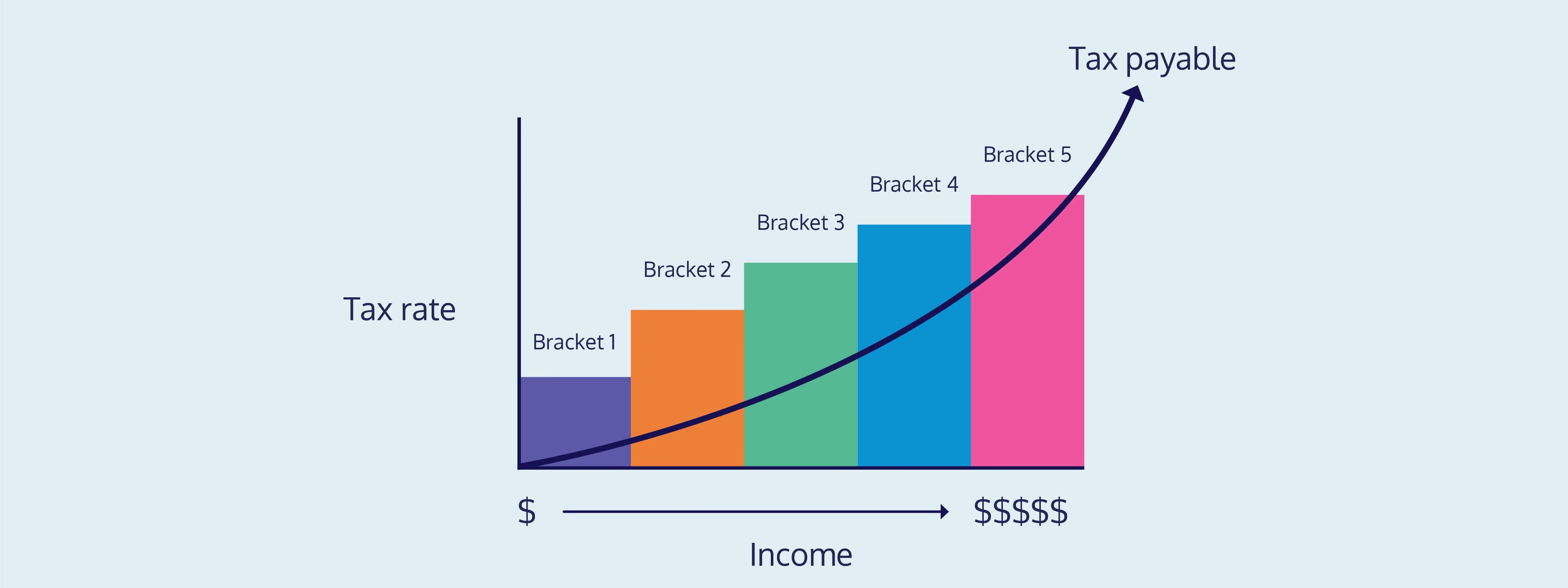

Other tax rates change depending on the circumstances. For example, income in Aotearoa is taxed progressively, meaning that the tax rate is different for different tax brackets. Which leads us nicely to:

What’s a tax bracket?

In New Zealand, income tax is a progressive tax, meaning that the more you make, the higher your overall tax-to-income ratio.

Income levels are split into bands or brackets, each taxed at a different rate. It doesn’t matter whether you’re a PAYE employee, business owner, or a sole trader – income tax brackets are the same for everyone.

Tax brackets and their corresponding tax rates are decided on by the New Zealand government, meaning they’re not set in stone. Different parties have different views on what fair taxation looks like, and economic factors (like inflation) can change the value of money to the point where the system doesn’t work as originally designed.

Although it doesn’t happen often, a new government could change the bracket thresholds (like in the 2024 budget), the tax rates, or even add a new bracket into the mix (like the top 39% tax bracket created in the financial year 2021/22).

Because of this, it’s a good idea to make sure you’re across the different tax rates and tax brackets each financial year – just in case.

Tax rates and thresholds for Financial Year 2026/27

| Taxable income | Tax rate |

|---|---|

| <$15,600 | 10.5% |

| $15,601 - $53,500 | 17.5% |

| $53,501 - $78,100 | 30% |

| $78,101 - $180,000 | 33% |

| $180,001 and over | 39% |

Source: IRD

💡 Looking for the old transitional rates? Check out our guide to the 2024 threshold changes.

How tax brackets and tax rates work

Income tax is calculated based on all your taxable income, whether you earn your income from a salary, a business, a side hustle, or any combination of the above. You’re required to pay income tax on every dollar you earn.

With that in mind, here’s where it gets complicated: Not every dollar you earn will be taxed at the same rate. This is where tax brackets come into play.

It’s a common misconception that your entire salary is taxed at the rate of the top tax bracket you qualify for, but this isn’t actually true. Instead, you only pay that rate of tax on income that falls within that tax bracket.

For example, if you earn $55,000 a year, you may think you need to set aside 30% for tax, which is $16,500. But our progressive tax rate system means that you actually pay 10.5% on the first $15,600 you earn, 17.5% on your earnings from $15,601 - $53,500, and 30% on anything over $53,501 (and under $78,100):

Bracket 1: 10.5% of $15,600 = $1,638 Bracket 2: 17.5% of $37,900 = $6,632.50 Bracket 3: 30% of $1,500 = $450 Total income tax bill: $8,720.50

This makes your effective tax rate 15.9%. Far less than paying 30% across the board!

💡 An effective tax rate is exactly what it says on the tin: the actual percentage of your total income that you pay in taxes.

Your effective tax rate is unique to your situation, and is a better metric for tracking your taxation levels than tax rates and brackets. It will vary depending on where your income falls within the bracket system – the closer you are to the top end of a bracket threshold, the higher your effective tax rate will be.

Sam and Ella are both freelance designers. Sam only recently started designing full time, and has a yearly income of $54,000. In contrast, this isn’t Ella’s first rodeo; she’s been at this a while, and makes around $77,000.

Even though both their annual incomes fall within the same tax bracket of 30%, Sam’s effective tax rate is 15.6%, while Ella’s is 19.9%. This is because only $500 of Sam’s income is taxed at 30%, in contrast to $23,500 of Ella’s income.

At the end of the financial year, Sam’s tax bill is $8,420.50. Ella’s tax bill is $15,320.50. Sam commiserates with Ella by taking her out for a beer. He picks up the bill.

💡 These examples use the rates and thresholds shown above. They don’t include ACC levies, student loan repayments, tax credits, or any PAYE already deducted.

📖 Curious about your own effective tax rate? Check out our tax calculator for sole traders!

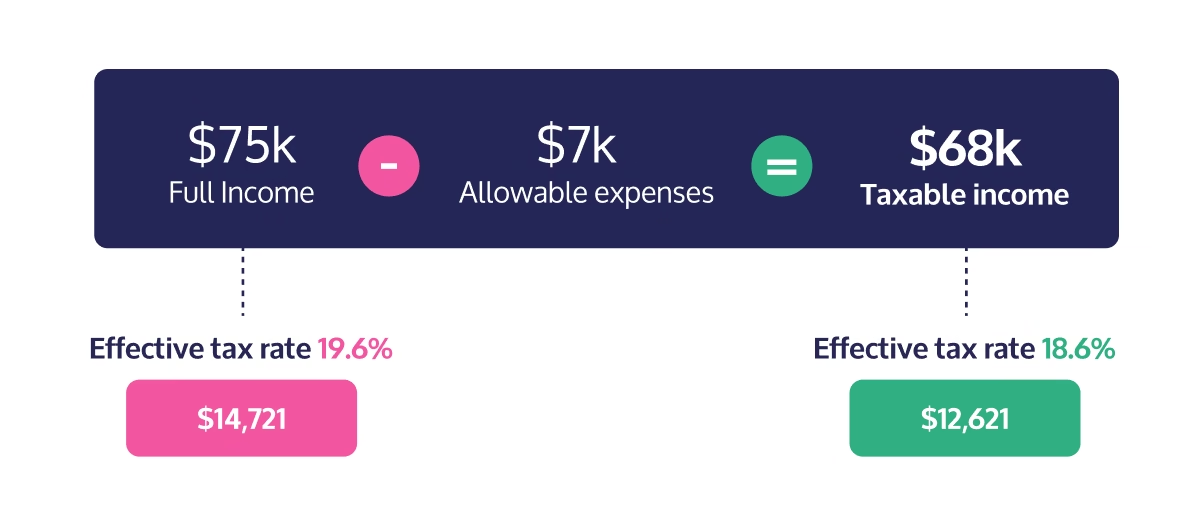

But wait! There’s actually some good news here, especially if you’re a sole trader. You can reduce your taxable income – and therefore lower your effective tax rate – by claiming tax deductions for approved business expenses (🎉).

How claiming business expenses affects your effective tax rate

To help sole traders and small businesses keep more of their money, Inland Revenue allows some business expenses to be claimed as tax deductions. What this essentially means is that you’re rewarded for putting money into your business – you won’t have to pay as much income tax come tax day. Win-win!

Here’s how it works:

- You purchase a good or a service that directly relates to earning your sole-trader income

- You claim the cost of the expense as a tax deduction

- The cost of the expense is excluded from your taxable income, which reduces the income you pay tax on and lowers your effective tax rate

- You pay less in taxes at the end of the financial year.

This is oversimplifying it – Inland Revenue won’t accept any and all purchases – but if you’re clever about it and the stars align, you could make a real difference to your final income tax bill.

After her surprise $15,320.50 tax bill, Ella is determined to reduce her effective tax rate.

Realising that her business could do with a refresh, she hires a freelance friend to help her revamp her brand and business cards. She starts advertising via Facebook, and invests in a few new tech subscriptions that save her time and effort (including Hnry!).

Ella also meticulously raises all her business expenses through the Hnry app, from little purchases like work stationery, to bigger costs like rent for her dedicated home office.

It all adds up. By the end of the next financial year, Ella has earned $75,000 in freelance income. But she’s claimed $15,000 in valid expenses. This lowers her taxable income to $60,000. Her tax bill is $10,220.50, making her effective tax rate 17%.

Ella takes Sam out for a beer. This time, it’s on her.

💡 This example uses the rates and thresholds shown above. It doesn’t include ACC levies, student loan repayments, tax credits, or any PAYE already deducted.

If your end-of-year tax bill is more than $5,000, Inland Revenue may require you to pay provisional tax for the following year. That doesn’t change your income tax rate, but it does change when you need to pay.

📖 Ready to raise more expenses? Find out everything you need to know in our monster guide to expenses.

📖 You can also use our tax calculator to see how claiming expenses could reduce your effective tax rate.

💡 If you’re not sure whether an expense will be accepted by Inland Revenue, it’s always a good idea to check with a tax specialist (like the Hnry team!)

How Hnry Helps

Hnry is a registered tax agent that can take the pain out of managing your taxes.

For just 1% +GST of your self-employed income, capped at $1,500 +GST a year, Hnry will automatically calculate, deduct, and pay your taxes, levies, and whatnot for you. This includes:

Our app models your income throughout the year and predicts your effective tax rate based on what you earn. We only ever deduct what we estimate you’ll owe, meaning you won’t get behind (or ahead!) on tax payments. You also won’t have to set money aside yourself - in fact, you’ll barely have to think about taxes at all.

Better still, using the Hnry platform costs less than using a traditional accountant, and is entirely tax deductible.

If that sounds good, join Hnry today and never think about tax again!