Life is a series of tipping points – that is, a point in time when the inconvenience of staying with the status quo outweighs the pain of moving.

Having spent eight years quietly growing my business, personal finance blog and podcast, The Happy Saver, I found that managing invoicing, expenses and tax obligations increasingly took up too much of my time. I had less and less to give to my core work: helping everyday Kiwis feel confident financially.

Ironically, I was becoming increasingly frustrated managing the financial side of a blog about money! Administration often interrupted the flow of my working day, yet I had zero idea if I was calculating my tax obligations correctly. I was right to be nervous; owing tax is no joke.

It was a clear tipping point; time to do something to take control of my financial admin. So, like many small businesses, my initial thought was to start using Xero…

- Using Xero as a sole trader/side-hustler

- Enter Hnry

- Switching to using Hnry

- Features for sole traders

Using Xero as a sole trader/side-hustler

Because my business was growing, my accountant had started hinting that it was high time I began using the accounting software Xero. I kept putting it off for two main reasons:

- I knew many sole traders who used it, yet still felt in the dark about the profitability of their business

- I didn’t want to introduce a new cost (a recurring software subscription) into my business

Plus, I was frustrated that despite my meticulous record keeping, until the end-of-year accounts were handed back to me for review, I never had a clear idea from my accountant of how profitable or otherwise I was.

While pleased The Happy Saver grew, I realised that Xero might be more than I needed. It was designed for much more complicated setups, but my business structure would always remain simple even if I were to 10x my annual income. I invoice clients for work done or get paid directly, pay automated expenses (such as software subscriptions) and make online or in-person purchases. That’s about it.

I asked around about Xero, and as people explained the intricacies of using Xero for their small businesses, I quickly concluded that I would be using a hammer to crack a nut, introducing greater complexity and cost into my business than I would ever actually need. Plus, I would have to set aside more time for administrative work than I thought necessary, and still need an accountant to tell me how much tax to pay.

In short: using Xero would make life easier for my accountant, but not for me.

Enter Hnry

My business model is good, simple, profitable, and can scale easily. I wanted to find an accounting solution that would help and not hinder my progress. So, I sought an alternative option, which is when I found Hnry.

I was looking for:

- A professional and standardised invoicing system

- A way to use expenses to offset future tax obligations in real-time

- Online storage of invoices and expense documentation that was IRD-compliant

- A reliable weekly income in my personal bank account, much like a PAYE employee

- Real-time data of gross income, expenses, and profit

- Info around how much I owe in tax and ACC levies

Again, I sought the crowd’s wisdom, and the conversations were surprisingly brief: “We love it, we should have switched to Hnry years ago.” I also read every article on their resources page. Finally, I spoke directly with one of their team. My thorough research made me confident that using Hnry would be the right decision for my business, so I signed up.

Switching to Hnry

I moved to Hnry during the tax year, which instantly removed one of my most significant expenses: my ever-increasing annual accountant’s fees.

It didn’t take long to get up and running – I could enter all of my invoices and expenses year to date, which was easy to do given I’d been compiling them monthly anyway. To ensure I was starting off on the right foot, I spoke with and emailed the Hnry team. All in all, Hnry’s user interface was intuitive and easy to learn. With everything in place, I went about my work.

But the real magic began once I had my feet under my desk, and began using Hnry daily. Within one minute of a client meeting’s ending, I had emailed them my invoice through Hnry, including a bespoke description of the work, the payment period and terms, and whether GST was applied.

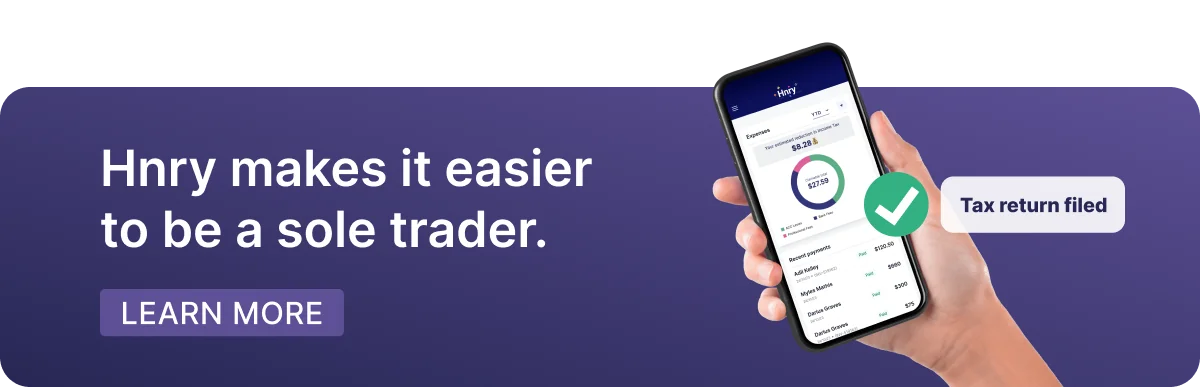

My Hnry dashboard clearly shows all outstanding invoices, and within a short time, I could see that my client had viewed their invoice and that payment was pending. This eliminates me wondering if they received my invoice.

Already, I had solved many of the issues I had with running my business, but once Hnry advised me that my client payment was made, giving me a clear description of how the payment had been allocated, my final question was answered. That question was: am I making any money?

Hnry had deducted income tax, ACC levies, and their small fee (which is applied to each payment, not as a monthly fee). My income after tax – what was mine to spend – was clearly shown.

(This happened even when I was paid directly, and not through an invoice – Hnry immediately deducts all taxes, etc from that, too.)

For the first time, I didn’t have to worry about setting money aside for taxes as it had all been taken care of!

Features for sole traders

Soon after issuing the first of many invoices, I also began uploading expenses into Hnry using their easy-to-navigate categorising criteria. I uploaded it on the go, literally standing in a shop, photographing the invoice, adding a few quick details, and uploading it! No more end-of-month scramble to find a missing receipt!

Within a day, the Hnry team reviewed this expense, applying it to my income and showing my YTD estimated reduction in income tax. They also provide clear feedback if I’ve miscategorised an expense, or wasn’t eligible to claim it.

Hnry has many additional features, meaning it can flex and fit a range of business types:

- It works for PAYE employees who also do freelance work

- You can send out quotes for your work

- They will chase up overdue invoices

- Additional income sources, such as investment dividends or PAYE income, can be added

- You can create allocations of money to future sick leave or holiday pay

- You can set up an automatic contribution to your KiwiSaver

- It can make additional contributions to old tax debt or your student loan

- You can allocate money to savings accounts, either business or personal

What Hnry has given me is, in many ways, the freedom to forget about the administrative side of managing a business and focus solely on the work I enjoy doing. It has given me my time back, particularly at month’s end. At any point, I can generate an income statement for this financial year showing my taxable income, income tax and ACC payments, and net pay. Knowing that I’m operating within the law regarding claiming expenses, payment of all tax obligations, etc., gives me great relief and has allowed me to draw more money from my business accounts than I felt comfortable doing before, simply because I know my true financial position. I know that the money in my account is now mine to manage.

Hnry has given me such clarity that it enabled me, for the first time and in real-time, to have some certainty over the reliability of this income. Until recently, I have always worked a part-time PAYE job because I was so uncertain about my actual business income. It has made me realise I’m doing better than I thought, allowing me to leave that job and focus solely on The Happy Saver, allowing me to try new things and make bolder choices than before.

Hnry is simply a game changer. My most frequent regret is that I didn’t switch to them years ago.